1980 Letter- Berkshire Hathaway.

1980 Letter- Berkshire Hathaway.

My key learnings from the 1980 letter written by Warren Buffet.

My Two Cents

1980’s buffet letters to shareholders, buffet initiated with Financial Reporting. He Describes reporting of Berkshire Hathaway as follows

Buffet wrote that many companies in his portfolio do not hold significant control (>50% stake) or not having a significant holding in that companies so buffet describes the GAAP reporting as follows.

In 1980, Berkshire Hathaway owns 60% of blue stamps. i.e above 50% of the holdings and it has significant control over blue stamps, Berkshire needs to report all the income, expenses in their books of accounts. I.e., In consolidated financial Statements with 40% interest of minority shareholders.

20-50% of the stake hold by the company is called as Investee companies. In this case, holding companies just state the earnings portion of what it is entitled from its subsidiary companies.

<20% of the stake hold by the holding company should record subsidiary dividend income as part of their P&L ( Income) if the subsidiary company declares Dividend and if not, no earnings of the subsidiary companies will be reported on Holding companies Earnings Report.

Buffet emphasize on the point of retaining earnings, he says he is not concerned if the company is paying dividend or not but he is more concerned that where do retain earnings is been invested into. Do these retain earnings are been invested into High return on capital business which generates more cashflows or it is been employed into return on capital which destructs they retain earnings over time?

Buffets Quotes – It is the act that counts. not the actors.

If the tree grows partially owned by us, but we don’t record the growth in our financial statements, we still own the part of the tree.

Buffet states that he greets the companies who use their retained earnings as a purpose of buyback of shares. The logic is too simple, Company announces the buyback because they know there are more worth than their current market value and shareholders get the best quote above the market price if participate in the buyback process

Sometimes the company does not have enough opportunities to reinvest their capital to generate higher ROCE compare to current ROCE. Eg. Hawkins, their growth has been stagnant because they don’t have much growth in the cooker industry and while diversification becomes the core when companies don’t forecast any growth in their own sector.

while if you don’t find good ROE business to reinvest your cashflows retained earnings deteriorate the ROE, it is better to distribute their Income Via Dividend or buyback of shares.

The competitive nature of corporate acquisition activity almost guarantees the payment of a full—frequently more than full price when a company buys the entire ownership of another enterprise. But the auction nature of security markets often allows finely-run companies the opportunity to purchase portions of their businesses at a price under 50% of that needed to acquire the same earning power through the negotiated acquisition of another enterprise.

After reading this, I remember one statement said by Madhusudan sir, In the stock market you can buy stock worth of 2 at 0.20 paise and can sell at 4, volatility is inevitable if you are in the market and so you need to work hard to get the core of when to buy and when to sell.

Buffet emphasis on real income. He quotes.

If you (a) forego ten hamburgers to purchase an investment; (b)receive dividends which, after-tax, buy two hamburgers; and (c) receive, upon the sale of your holdings, after-tax proceeds that will buy eight hamburgers, then (d)you have had no real income from your investment, no matter how much it appreciated in dollars. You may feel richer, but you won’t eat richer.

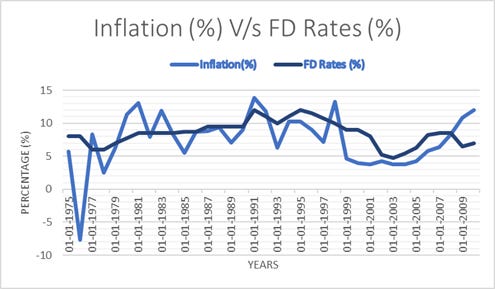

Many investors emphasise on the nominal rate of return rather than Real Return.

In India, Average Inflation for 1975-2010 is 7.5 and FD Rates 8.5. and the median is 8.01 and 8.5.

Many millennials think about parking their surplus money in FD while parking your funds in FD is not creating wealth. Your inflation eats all your savings and your real return is minimal.

For capital to be truly indexed, return on equity must rise, i.e., business earnings consistently must increase in proportion to the increase in the price level without any need for the business to add to capital—including working capital employed. (Increased earnings produced by increased investment don’t count.) Only a few businesses come close to exhibiting this ability.

In this buffet talks about the business who has a moat. E.g. maggie, Nestle has a very strong brand recognition of maggie, it constantly chug out cash without increasing their working capital. It has a strong demand and market presence which holds 66% of the market share in noodles segment.

Moving ahead buffet talks about turnaround and he quotes that “turnaround seldom turn Around”

He says there is one in a million opportunity where you get good business at a very low price. You need to be expert when you are buying and need a lot of patience and conviction for the business to turnaround.

We conclude that, with few exceptions, when a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

Ahead Buffet states about the selling of bonds by the Insurance Companies to underwrite their policyholder’s claims. Insurance is a very volatile and uncertain business, you don’t have any idea about the claim by the policyholders and in the distressed situation of insurance companies, they sell their bonds to repay their policyholders.

While there are two ways Insurance companies can pay back to their policyholders.

1. Sell the longterm bonds like 10,20,30 years of bond and booking hefty losses and pay to policyholders which reduces the retained earnings by a large portion which deteriorates the value for the business and also reduces the claims.

It reflects three events for the business

a. Price sensitive and short term policyholders switch to a near competitor.

b. Due to a, there will be a shrink in the new premiums and also reduces uncertainty due to the reduction in short term policyholders.

c. Asset Liability Mismatch.

2. Sell the stocks which are quoting above the cost price and hold the losers hoping to be profitable in future and sell the bonds which are purchased in the near term this will not hamper the earnings in the short term, but it shows a negative sign in the long term perspective

You know which option hurts you more.

On a concluding note, I want to share one quote shared by warren buffet which helps me while investing.

The forecasts may tell you a great deal about the forecaster; they tell you nothing about the future

If you like this blog piece, please hit the subscribe button so Equitymaniac can direct reach to your mail and you don’t miss any future blog post by us.

Let your friends and family know how cool we are😅

Thanking for Reading,

Equitymaniac.

Happy Investing.