All about Mutual Funds-II

All about Mutual Funds-II

As promised we are back with our part II. In this part, we will discuss all the schemes related to debt instruments in Mutual funds. ( If you haven't read our part I please Click).

Many of the millennials have just started their career and they have just availed their first salary credited in their bank account, they are really happy and they want their dreams to fulfilled like buying a smartphone, going for a trip, partying etc., but it is truly important to save the money in the initial phases. Many millennials are worried that they don't lose out their hard-earned money in this stock market. Initially, I advised to invest in equity mutual funds but if you still don't have confidence in the Equity related funds I would suggest investing in Debt related Mutual funds. So what are debt-related mutual funds and what are the returns you can expect from debt rated funds? So let's Understand.

Income/Debt Oriented Schemes

1 Overnight Fund

2 Liquid Fund

3 Ultra Short Duration Fund

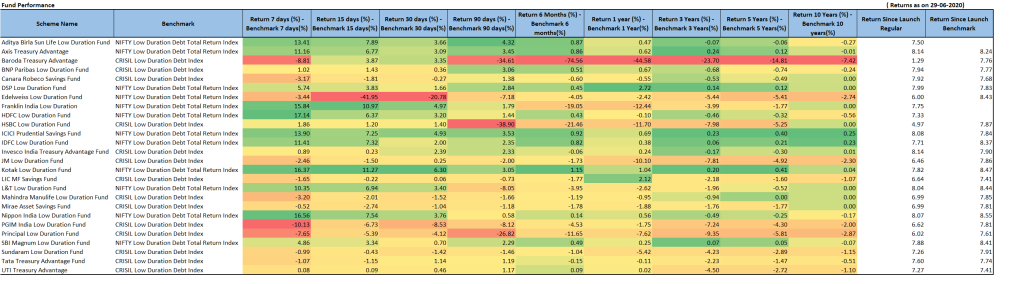

4 Low Duration Fund

5 Money Market Fund

6 Short Duration Fund

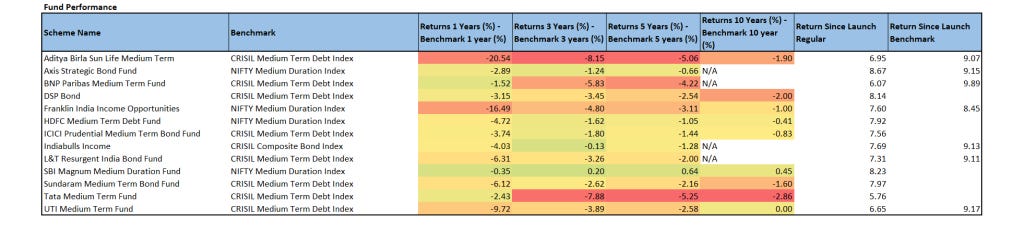

7 Medium Duration Fund

8 Medium to Long Duration Fund

9 Long Duration Fund

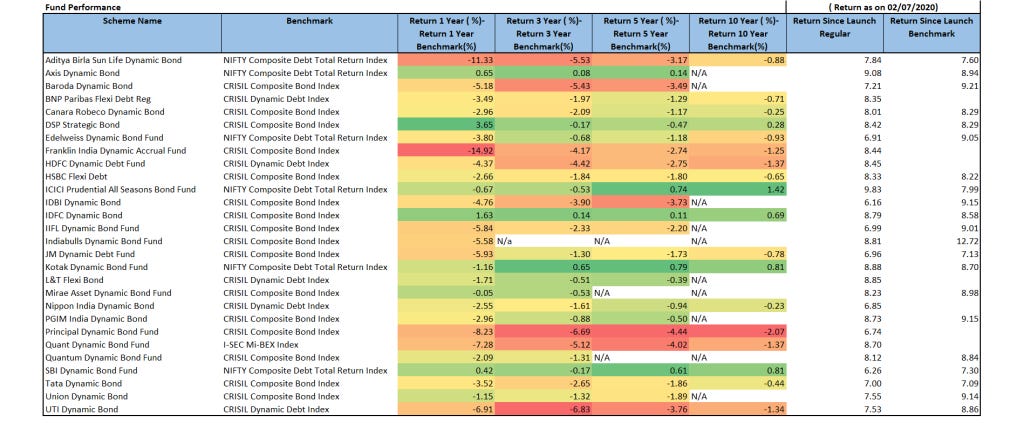

10 Dynamic Bond Fund

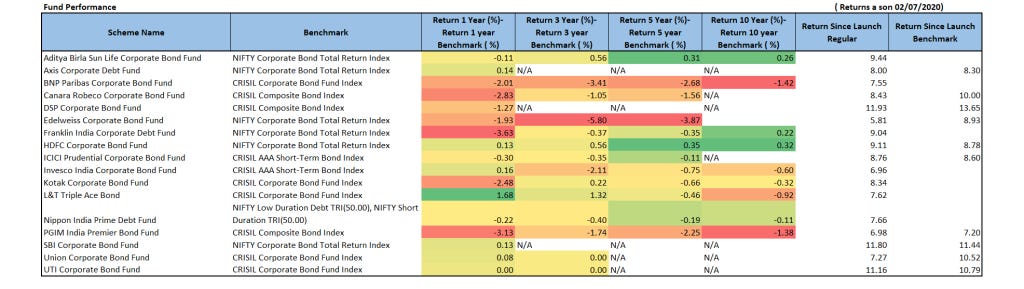

11 Corporate Bond Fund

12 Credit Risk Fund

13 Banking and PSU Fund

14 Gilt Fund

15 Gilt Fund with 10-year constant duration

16 Floater Fund

Overnight Fund

Overnight funds invest in CBLO's Reverse repo rate and other money market instruments which held to investments only for one day.

Overnight funds invest in CBLOs( Colaterised borrowing and lending Obligation), overnight reverse repos, and other debt or money market securities that mature in one day. This is in keeping with SEBI norms, which requires them to invest only in assets with overnight maturity.

The entire asset holding of an overnight fund can be classified as "Cash and Cash Equivalents". The portfolio of an overnight fund is replaced every day with new overnight securities. Overnight schemes are not permitted to invest in deposits or specified risky debt instruments

Overnight funds earn only through interest payments on their debt holdings. There is no scope for earning capital gains as the securities held by the fund mature in one day. In fact, returns of overnight funds reflect overnight lending and borrowing rates. When interest rates are falling, and short-term liquidity is abundant, overnight rates in the money market decline. When interest rates are rising, and market liquidity is tight, overnight rates increase. Thus, returns of overnight funds are closely linked to rates and conditions in the overnight market for funds.

Overnight funds are extremely secure and very small chance of default which makes almost a secure investment. You can expect 4-5% Return p.a. In this funds, Expense ratio is too low and you can park your funds as and when require and redeem as per your convenience.

Liquid Funds.

Liquid funds aim at providing a high degree of liquidity and safety of the capital to investors. For this reason, the fund manager invests in high-credit quality debt instruments. The allocated proportions are as per the fund’s investment objective. The fund manager will ensure that the average maturity of the portfolio is less than 91 days.

Liquid funds invest in Treasury bills, certificate of deposit and commercial paper which are a highly secured and very less risky investment. You can expect 7-9% return p.a

Liquid funds are an excellent option to park your idle money. These are low-risk havens which offer higher returns than a savings bank account. Liquid funds try to emulate the liquidity aspect of a savings bank account. These funds don’t have exit loads. It gives you the freedom to withdraw funds as per your convenience.

Ultra Short term Duration Funds

Ultra-short-term funds can be linked to be close cousins of liquid funds. These funds offer more liquidity than any other class of funds with long investment horizons. According to the rules set by the Securities and Exchange Board of India (SEBI) for liquid funds, it has been decided that such funds can invest only in securities that mature no longer than 91 days. However, these rules do not apply to ultra-short-term bond funds.

These bonds can, therefore, invest in securities that mature both before or after 91 days. Typically, the investment horizon for these ultra-short-term funds ranges from a week to about 18 months. Hence, if you have surplus funds that you wish to park for 1 month to 9 months and earn some dividends from, then this investment vehicle can be the one you are looking for.

The only risk associated with this funds is interest rate risk as because of the short term maturity of underlying assets. you can expect an average return is 7-9% p.a.

Low duration Fund.

To understand the low duration fund, we have to understand what a duration Is?

The duration of a debt fund measures how much the fund's value fluctuates in response to changes in market interest rates. Duration is also known as interest rate risk. Therefore, the higher the duration, the more volatile the fund value, and the greater its interest rate risk. Calculating duration is quite tedious and requires a complex formula and detailed data on the fund's investments. For most investors, a good thumb rule is to estimate duration based on the maturity of bonds held by the fund.

Funds holding long-maturity bonds have higher durations as compared to funds that hold shorter maturity bonds.

If a fund increases its holdings of long-term bonds, the duration of the fund increases, as does its interest rate risk.

Money Market Fund

A money market fund is a kind of mutual fund that invests only in highly liquid near-term instruments such as cash, cash equivalent securities, and high credit rating debt-based securities with a short-term, maturity—less than 13 months, such as U.S. Treasuries. As a result, these funds offer high liquidity with a very low level of risk.

They mainly invest in Bankers acceptance, Certificate of deposits, Commercial papers, Repurchase Agreement and US Treasury. This is not as safe as cash but leads to very low risk and volatility of interest rate risk.

Short Duration Fund

Short-term bond funds invest in securities that have a maturity period between a year to three years and offer high liquidity. Apart from commercial papers and certificates of deposit, these also invest in government securities and medium and long-term instruments. Any entity or fund house can issue short-term debt (bonds) including government, corporations for investment and companies rated below investment grade. These are also available in dividend and growth options.

These funds provide a better yield and good return for the investors who want to park their funds for short to medium period of time. Interest rate risk plays a vital role in the performance of these types of funds.

Medium Duration Fund

Medium Duration Funds invest in debt securities and money market instruments so that the Macaulay Duration of the fund’s portfolio is between three and four years. Hence, these funds are recommended to conservative investors with a four-year investment horizon. Medium Duration Funds have a higher maturity than overnight funds, liquid funds, ultra-short duration funds, low duration funds, money market funds, and short duration funds but lower maturity than medium to long-duration funds and long duration funds. These funds are best suited for investors who want to meet certain financial goals in 3 years and are a good alternative to bank deposits. The average returns of these funds range between 7 and 9%.

A medium duration fund is basically a debt fund. Hence, like all other debt funds, these funds also carry the three risks – credit risk (or the risk of default by the issuer), interest rate risk (effect of an increase or decrease in interest rates on the value of the fund), and liquidity risk (of the fund house). Hence, it is important to ensure that you analyze the portfolio to ensure that the fund invests in high-quality debt securities so that the credit risk is negligible. Also, research the fund manager and check how he has performed through different interest rate regimes. An experienced fund manager can help you weather the storm of a rising interest rate period optimally.

Medium to long term duration

Medium to long term Duration Funds invests in debt securities and money market instruments so that the Macaulay Duration of the fund’s portfolio is between Four to seven years. Hence, these funds are recommended to little bit aggressive investors with a seven-year investment horizon. Medium Duration Funds have a higher maturity than medium-term bonds funds, overnight funds, liquid funds, ultra-short duration funds, low duration funds, money market funds, and short duration funds but lower maturity than and long duration funds. Risk and reward are expected on the convexity and volatility of interest rate risk.

Long Duration Bond

This is a similar type of funds like medium to long term bond. the difference is only the maturity of the bond the maturity rises to 10-year duration bond and riskiness increases due to maturity and interest rate risk.

Dynamic Bond

Dynamic Mutual Funds have a ‘dynamic’ maturity as well as composition. These funds have an investment objective of delivering optimum returns in falling as well as rising market cycles. The fund manager of a dynamic debt fund manages the portfolio dynamically with respect to the changes in the interest rates.

Talking about interest rates, it is important to note that there can be pauses between interest rate changes. These pauses can affect the returns on bonds too. Hence, Dynamic Mutual Funds are a good option for investors who want to generate returns from their bond investments regardless of the interest rates.

The important feature of a dynamic fund is that it switches between short-term and long-term securities in n time. So, if the fund manager feels that the interest rates are about to drop, he switches to long-term bonds. On the other hand, if he feels that the interest rates have reached the lowest peak and will only rise from here, he safeguards his losses from long-term bonds by switching to short-term bonds. This helps help iron out the creases caused by abrupt interest rate changes. Further, the fund manager of a dynamic debt fund also invests in gilts or corporate bonds depending on his expectation of the interest rate change.

Corporate Bond Fund

A corporate bond fund is essentially a mutual fund which invests more than 80% of their total financial resources in corporate bonds. Business organisations sell these to fund their short expenses, such as working capital needs, advertising, insurance premium payments, etc.

Corporate bond funds are increasingly becoming the popular debt instrument for businesses to raise required finances as associated costs are lower as compared to bank loans.

Corporate bond mutual funds have lower risk sensitivity as it is a debt instrument ensuring capital protection. It is ideal for risk-averse people looking for high returns on their investments. The time period of the top corporate bond funds generally ranges between 1 and 4 years, preserving liquidity of the investor.

Since the market fluctuations have a higher chance of occurring in the long run, these debt funds try to operate in the short term to avoid such market volatility. This makes a corporate bond fund a more attractive option over government bonds, which have longer tenors.

Another benefit of investing in corporate bond funds over government funds are the higher interest rates payable on the former. However, government bonds are more stable, as it has negligible default risks. The risk on corporate bonds, on the other hand, depends on investment patterns followed by the respective portfolio managers. Companies with high credit ratings have low chances of defaulting, while the ones with relatively lower ratings have a higher risk factor.

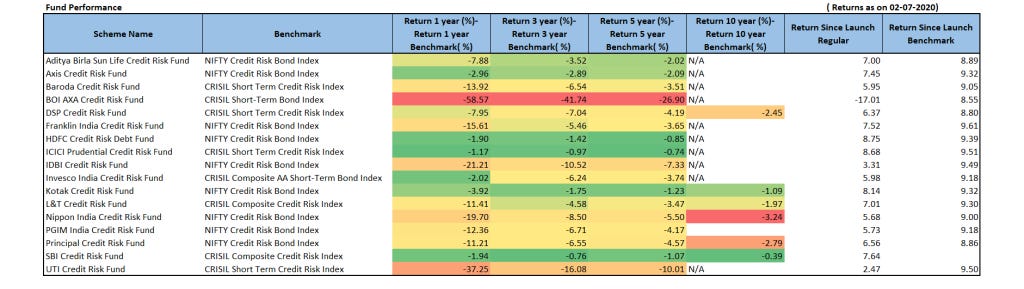

Credit Risk Funds

Credit Risk Mutual Funds are debt funds which invest in low-credit quality debt securities. These funds have higher risks since they invest in low-quality instruments. Securities with a low credit rating tend to offer higher interest rates. Usually, instruments with a credit rating below AA are considered to carry a higher credit risk. The fund managers of Credit Risk Funds also choose securities which might get a boost in rating (as per their analysis). This can have a positive impact on the NAV of the fund. As a retail investor, you should be very careful while selecting the fund and investment horizon.

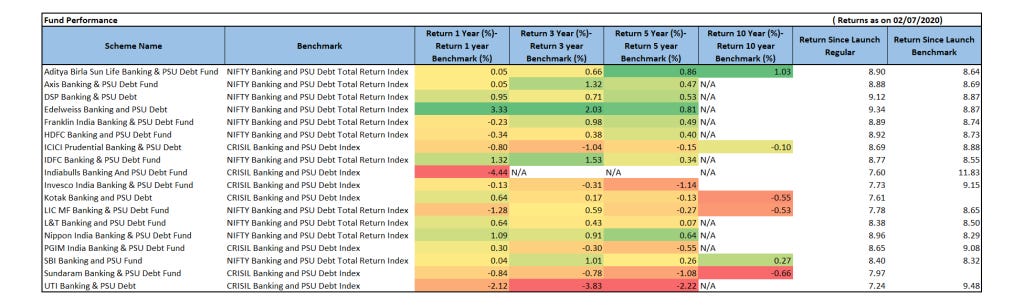

Banking and PSU funds.

Banking and PSU (public sector undertaking) debt funds primarily invest at least 80% of their corpus in obtaining debt instruments issued by banking institutions and other public sector companies. As per a recent amendment announced by SEBI in December 2017, debt securities issued by municipal bodies can also be included in the portfolio of such a banking and PSU fund. Such listed companies are usually large-cap and have AAA- rating from the top credit rating agencies in the country.

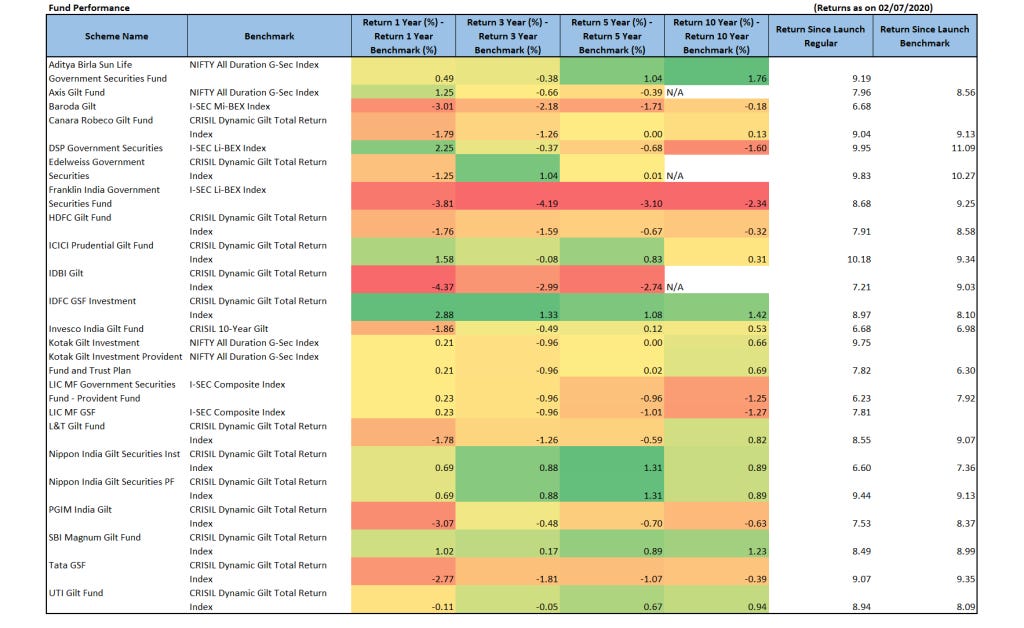

Gilt Fund and 10 year Gilt Fund

Gilt mutual funds primarily invest in securities issued by the Reserve bank of India to fund government operations.

The primary function of the central bank is to act as a banker to the government. Both central and state units can approach the RBI if they require additional funds to meet operational expenses. The central bank, in turn, issues interest-bearing bonds, which it sells to the residents in exchange for funds. These bonds come with a fixed maturity period, after which investors are disbursed the corpus amount along with proposed interest rates. Mutual funds comprising such government-mandated security are known as gilt funds.

Difference between gilt funds and 10-year gilt funds is maturity. A gilt fund with 10-year constant duration entails a fixed maturity period of 10 years and is suitable for long term investment schemes for individuals having a lower aptitude for market risks.

Gilt Fund Returns- Benchmark return

10 Year Gilt Fund return- benchmark

Floater Funds

A floater fund majorly comprises debt securities which provide a varying rate of returns depending on market fluctuations or benchmark indices. Hence, investors can benefit from fluctuations of the business cycle, as it affects the returns generated by standard stock market instruments significantly.

Such mutual funds aim to mitigate the risk factor by primarily investing in debt tools such as corporate bonds, treasury bills, certificates of deposit, etc. as they pose as a liability to issuing entities.

The rate of return on investment generated by a floater mutual fund is heavily influenced by market fluctuations of interest rates. Any change (an increase of decrease) in the repo rates set by the Reserve bank of India affects the prevailing return rates of zero risk securities, as well as bonds issued by the government and public limited companies.

A rise in the repo rate (the rate at which scheduled commercial and public sector banks procure loans from the RBI) indicates an increase in the returns generated by zero risk instruments and government bonds, thereby increasing the yield of a debt floater mutual fund.

Thus, an increase in the market lending repo rate increases the returns generated by all market-linked debt securities, respectively. Investing in a floater debt fund, which primarily consists of such instruments, is subject to fluctuating yields and correspondingly fluctuating NAV, as per market changes in interest rates.

Conclusion

Even in this, you visioned that majority of the funds have outperformed the benchmark but while some funds have so underperformed that it eroded the capital of the investors in this debt fund, so our advice is to always consult your financial advisor because they will help you to select the best funds for you and help to protect and appreciate your capital.

This brings us to the end of part II.

If you have any questions related to debt or equity funds please free to contact and we will soon release our part III.

Thanks for Reading,

EquityManiac

Credits and Sources : AMFI and google Sources