Hope you all are well and safe, after a long time we are posting research on a specific company, we are sorry, due to our time constraint and some credit you can give to procastination as well, but now we are charged and gaining back the confidence of our readers.

CanFin Homes

Market Cap-7123Crs

Free Float-4986Crs

Industry trend

The housing finance industry is dependent on the growth of the real estate sector, so the real estate sector comprises four sub-sectors - housing, retail, hospitality and commercial. The construction industry ranks 3rd among the 14 major sectors in terms of direct, indirect and induced effects in all sectors of the economy. The real estate sector in India is expected to reach a market size of US$ 1 trillion by 2030 from US$ 120 billion in 2017 and contribute 13% to the country’s GDP by 2025. Indian real estate is expected to increase by 19.5% CAGR from 2017 to 2028. After the unlocking process was initiated in the third quarter of 2020, both the residential and office markets started showing promising signs of revival.

Home sales volume across eight major cities in India jumped by 2.5x to 33,403 units from July 2020 to September 2020, compared with 9,632 units in the previous quarter, signifying healthy recovery post the strict lockdown imposed in the second quarter due to the spread of COVID-19 in the country. The government of India along with the governments of respective states has taken several initiatives to encourage development in the sector.

The Smart City Project, with a plan to build 100 smart cities, is a prime opportunity for real estate companies.

Below are some of the other major Government initiatives:

· The Atmanirbhar Bharat 3.0 package included income tax relief measures for real estate developers and homebuyers for primary purchase/sale of residential units of value (up to 2 crores from November 12, 2020, to June 30, 2021).

· In October 2020, the Ministry of Housing and Urban Affairs (MoHUA) launched an affordable rental housing complex portal.

· To revive around 1,600 stalled housing projects across top cities in the country, the Union Cabinet has approved the setting up of a 25,000-crore alternative investment fund (AIF).

· Under Pradhan Mantri Awas Yojana 1.12 crore houses have been sanctioned in urban areas, creating 1.20 crore jobs.

· The government has created an Affordable Housing Fund (AHF) in the National Housing Bank (NHB) with an initial corpus of 10,000 crores (US$ 1.43 billion) using priority sector lending shortfall of banks/financial institutions for micro-financing of the HFCs.

· Responding to an increasingly well-informed consumer base and bearing in mind the aspect of globalisation, Indian real estate developers have shifted gears and accepted fresh challenges.

· The most marked change has been the shift from family-owned businesses to that professionally managed ones.

· Real estate developers, in meeting the growing need for managing multiple projects across cities, are also investing in centralised processes to the source material and organise manpower and hiring qualified professionals in areas like project management, architecture and engineering.

· Residential real estate in the country’s top seven property markets has staged a comeback with sales exceeding pre-pandemic levels, driven by record-low interest rates, discounts offered by developers, lower prices and stamp duty cuts in key areas.

· The improved sales momentum has lifted confidence among realty developers, pushing them to launch more projects as indicated by the rise in new offerings across markets.

· As the above image states the recent quarter update above the real estate which differentiated between the affordability and budget segmentation for the residents in their individual’s cities, as we know that Canfin homes focus less than 40 lacs loans while the budget fragmentation is visible with Kolkata, Delhi (NCR) and other cities. This can be a huge runway for growth in Tier1 as well Tier 2-3 cities.

· Indian population is gradually shifting to metro cities and non-metro cities for the sake of increasing lifestyle, more employment, better education for children. These are the certain reasons which rapidly increasing the urban population, as we can see in the below chart there is an estimate of 52.5 crore population can be living in the urban cities and that could be a good reason to justify the growth in the industry as well consumption of home loans.

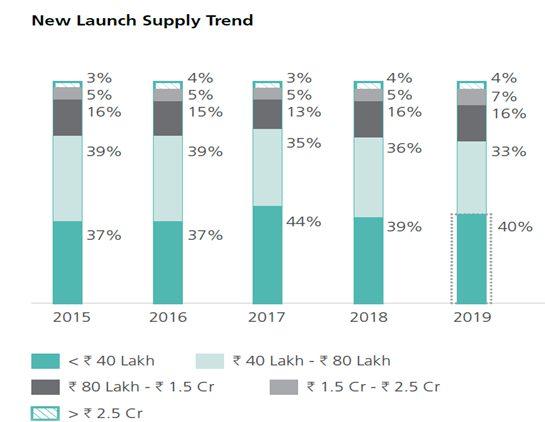

· There is a constant supply trend of affordable housing in real estate. More than 40% of the new houses are in the range of fewer than 40 lacs taking care of population earning capacity and affordability.

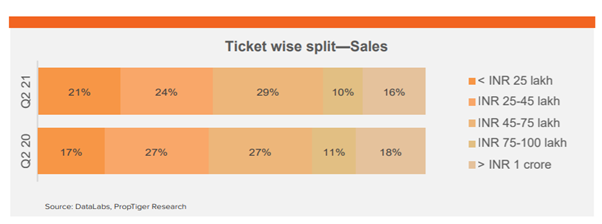

· If we check the quarter data, there is clear visibility of increasing sales of homes (residents) of less than 25 lacs. Permanent working from home culture has been positively impacted a sudden demand in Tier 2 and Tier 3 cities as well.

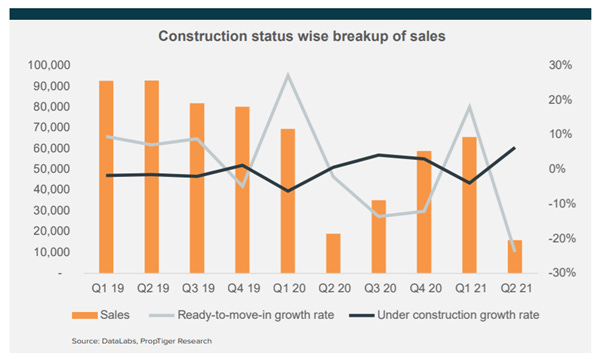

· As of June 2021, we can verify that in metro cities sales of the new residents is been decreasing and under construction growth is been increasing with a pacing rate, to justify many promptly want to invest in new space as the stamp duty, government subsidies and schemes push few individuals to buy or invest in few schemes to get better returns at a lower cost which realise the uptick in demand and better returns that can be fetched against other investments.

The Total Market size of financing is 14,00,000 Crores, while it is distributed as the image stated below.

Housing finance is a major constituent in the market size, due to the increasing population and aspirants to move to a new city and achieve their dreams. These aspirants are more job seekers and to establish their life for lifestyle and giving better future for the generations.

About the Company

· Canfin Homes Ltd, a housing finance company promoted by Canara bank, in 1986. The first canfin was founded by B Ratnakar, objective was to promote homeownership & increasing housing consumption in the country. In the initial years, the shareholders of the company were Canara Bank, HDFC, UTI and Bank financial services.

· CanFin homes is one of the few NBFC that has the licence to take deposits from the public.

· This company made a Debut in the year 1991 and performed outstanding from few decades. The company mainly focus on housing loans to individuals specifically lower- and middle-income group. Canara has always focused on the salaried class that will be Govt. and Cat A class for decades, now they also distribute to CAT B and C as well.

· The company is headquartered in Bangalore, they have a pan presence having 186 Offices and 14 satellites offices which covers 100 cities across 21 states & Union Territories.

· Canfin Homes still gets 70% of the revenue from south India they have a strong grip and evidence of growth in south India,

· They have the highest rating from the credit rating agency with AAA of long-term borrowings which impacts to get borrowings at a lower rate which can be a competitive advantage against other HFC’s.

Key Milestones to note. Year Achievements 1987 1st branch of Canfin Homes at Jayanagar, Bangalore 1988 Opened the first branch outside south India at Delhi 1991 Loan Book size crossed Rs. 100 Cars 2012 Disburse Rs 1000Crs, 50th branch opened at NCR 2013 Loan book size crossed 10,000 Crs 2014 Operating profit crossed at 100 CRS, Opened 100 Branch at Begur 2015 Net profit crossed 100 Crs mark, Raised 276 Crs capital under right Issue

2018 Runner Up in NBFC cat by Fe India’s best banks awards, Canfin homes made its foray into the states of Punjab and West Bengal

2019 Loan book Crossed 19000 Mark, Foray into the distribution of general insurance products through corporate agency 2021 Loan Book Crossed Rs22000 CRS Benchmark

Financials

Comments

Total loans are growing at an average of 21% and median at 18%. Management is still bullish on the growth and can fin homes can grow at 15% Cagr for the next 5-7 years

· Housing loans is constant at 89% average, while due to pandemic there is very little demand for the housing loans for the year and to maintain the market share and increase profitability management is focusing on the LAP, mortgage loans and developers’ loans.

· Canfin Homes has a proven track record in maintaining and stabilising the NPA’s, we can see that NPA on average is 0.47% and median NPA is 0.43% that is the classic example of risk management.

· Canfin homes also stand strong in Net NPA’s.

· Assets of Housing loans and Non-housing loans also grew simultaneously.

· There is constant growth in branches and employee count. The branch has expanded from 83 to 200 and while the employee count has been increased from 387 to 1000.

· NII has a constant grip at 3.25% and while the median is at 3.35%. Management commented they will maintain 3.4% NIM for the next few qtrs.

· Net profit has an average growth of 31%.

· We can clearly state that ROA is constantly at an increasing stage and the Cost of borrowings is at a decreasing rate which positively impact the spreading growth and profitability for the company in upcoming years.

· The average revenue per employee and average revenue per branch is constantly increasing which shows the strength has been maintained in the company.

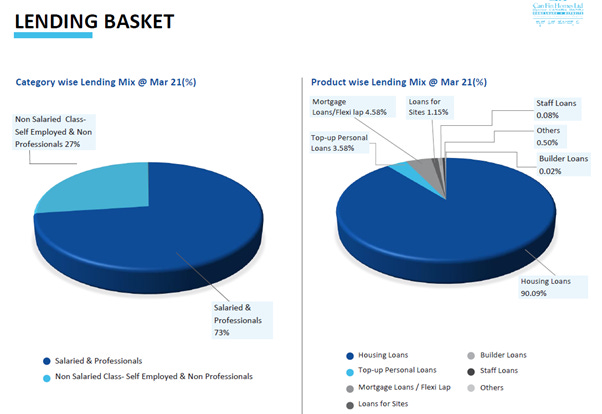

Lending Baskets

· We can Identify that Can fin Homes is constantly been focusing on housing loans. As the above image states that more than 90% of the loans are disbursed to housing loans and the other 10% is distributed in top-up loans (3.58%), Mortgage loans (4.58%), Loans for sites (1.15%), staff loans (0.08%), Builder loans (0.02%) and rest to others.

· In housing, loans Can fin homes have constantly focus on the salaried & professionals which constitute 73% of the portfolio and 27% Non-salaried persons which majority include self-employed.

· While from Q42021 the management has taken initiative to change the style for a few qtrs. where salary constitutes 83% while they have tended to focus more on developers’ loans and LAP loans.

Funding Baskets.

· The most important for any NBFC is to focus on the liability side, that’s how it creates the strength, the CanFin Homes have built the liability side from market Borrowings (Issuing bonds, NCDs) and other deposits. The bank borrowings constitute 51%, market borrowings at 26%, NHB at 21% and deposits at 2%. This is the last few years how the canfin is building up the liability side and operating at a lower cost with a proven track record and trust which helps them to raise at a lower rate and lend at a cheaper rate.

Management

· Bharti Rao (Chair Person)

Bharti Rao is a post-graduate degree holder in Economics (M.A.) and Certified Associate of Indian Institute of Bankers (CAIIB). She has more than 43 years of experience in the banking industry, has held domestic and international positions, and was in charge of Project Finance, Credit & Risk Management, International Banking, Human Resources, Mergers and Acquisitions. Served as the Deputy Managing Director of SBI and she had held concurrent charge of SBI’s 7 Associate Banks and 7 Non-Banking Subsidiaries.

· Girish kausgi (Managing Director & CEO)

Shri Girish Kousgi is a graduate in Commerce (B.Com.) and Postgraduate in Business Administration (MBA). Shri Girish Kousgi is a Banking professional with 25+ years of experience. He has extensive experience in managing assets and liabilities and has gained expertise in mortgage, retail lending, SME and Agribusiness.

He has worked in HDFC Ltd., ICICI Bank, IDFC Bank, and Tata Capital during his career so far.

· Shreekant M Bhandiwad

Shreekant is a Post Graduate in Agricultural Science viz., M.Sc. (Agri) and a CAIIB. Shreekant during his service in the Bank he has headed different branches, Circle Offices and various departments at the Circle and Corporate level. Shreekant is a senior banker with 26 years of commercial banking experience having served across the States of Haryana, Rajasthan and Karnataka.

He has significant experience in retail banking for over 16 years in Bengaluru, Hyderabad and Kerala apart from an experience of about 11 years in credit risk including risk-based verification strategies for loan products, measure credit expansion opportunities in the lending market and validate and implement credit risk models.

· Shri Debashish Mukherjee (Director)

Debashish is a post-graduate in Business Administration (MBA - Finance) from the University of Kolkata. He started his career with Punjab National Bank as a Financial Analyst on scale II in 1994. He joined the United Bank of India as an Asst. General Manager (Credit) in the year 2006.

He is overseeing the functions of Risk Management (including Capital planning), Financial Management and subsidiaries, MSME, Credit Administration & Monitoring, stressed Assets Management and Recovery, Inspection, Treasury, International Operations & Corporate Customer Relations.

· Satish Kumar Kalra (Director)

Satish Kumar Kalra has been a Member of the Advisory Board for Banking and Financial Frauds since March 2020

He has wide experience in the areas of Treasury Management, Risk management, Corporate Planning, Inspection & Audit, Merchant Banking, Board Secretariat, Credit Monitoring & Review, Recovery Management and Legal, Retail & MSME lending. He has experience of about 38 years in the banking industry.

Comments

· In relative valuation, we can indicate that Camfin Price to Earnings( P/E) is 15.8X, while other companies like Home first and Aavas financiers is trading at 50.1x and 77x, Aavas and Home first price to earnings is not sustainable on a long term basis. If we compare the ROA and sales growth with the PE there is a positive correlation between both of these as the financing business has adequately been analysed on ROA. With ROA and ROE, the Canfin homes are perfect positioned in valuation terms. Canfin homes price to earnings is justifiable due to proven track record and having a parentage advantage.

· While among the price to book it is trading at 2.76X. On Price, to book the valuation looks stretch ( at certain you can give credit to bull run as well)

· Return on equity is 19.2% which is the top leading compare to other HFC’s.

· Return on Assets is 2.12% but which is stable for the years. (why this we talk in the analysis section)

· Sales growth is 13.3% CAGR for 5 years which is still favourable comparing with LIC Housing, REPCO and India bulls.

Analysis

· Before we start with the analysis part, I briefly want to add what are some important parameters which I seek before Investing in any HFC’s

· The most important for any HFS’s is “Management, Management and Management”

· The second most important thing is to manage the risk with profit and sales growth.

· So, as we have raw materials in the manufacturing companies, procuring money for any Finance company is the raw material, how cheap they can borrow and how costly they can lend is the whole game of the HFC’s.

Now, what are the propositions which help to procure the money?

· 1) Proven Track record (HDFC, Canfin)

· 2) Brand Image and Brand Loyalty

· 3) Parentage Advantage.

· While all the above 3 helps the Canfin homes to get the money at a lower rate and that’s why the cost of borrowing is just 6.87% which is exceptionally good.

· CanFin homes have an 83% (now decreased to 82-80%) of the portfolio consists of salaried person which is mostly B, C and D category because they have a stiff competition to lend at A category loans. They agree to take a quite bit of risk due to maintaining the spread and increasing NIM, you can check the risk profile and the lending rate between the salaried and the self-employed.

· During the 2014-15 Scenario when HFC’s were giving a good chunk of loans to developers, while can fin homes stayed conservative and lost the support of shareholders taking as a negative sentiment, but when the DHFL fiasco happened, shareholders acknowledge the purpose of risk management and can fin stick to its core motives which made the can fin homes more trustworthy and increased the loyalty for the shareholders.

· So HFC’s is more focused on maintaining the risk, stabilising and conservatively increase the profit while in this scenario they started to lend more towards the developers loans due to maintaining the market share and there is low push demand from the salaried category, They are focused to bit aggressive for next 3-4 Qtrs. to maintain and try to take the leap of growth which can take the yield upto10-10.5% which can be impressive for the company with such a favourable global scenario.

· 22% of the salaried portfolio can be into rerating of interest amount due to decrease in interest rate, in my view that wouldn’t impact much.

· Target ticket Size has been increased from 18 to 20 lakhs, which helps to focus on few other segments that will help grow the book without taking an incremental risk.

· So overall with the strong management, strong fundamentals and strong execution with the growing book at 15% or more, having a target of 35000 loan books in the next 2 years with this optimistic and upcoming demand in housing and can make a good bet for 3-5 years.