Sirca Paints- Kyuki hum diwaaro pe nahi rehte to Ghar hai Aapse

Sirca Paints- Kyuki hum diwaaro pe nahi rehte to Ghar hai Aapse

let's see the industry structure and risk for the company in the upcoming years and let's see is this company worth investing in or not.

We are pretty well known with all the large-cap companies like HDFC Bank, Titan, Asian Paints, Bajaj Finance, Maruti Suzuki. They are the leader in their industry commanding good moat for the business and having a good market share in their industry but I want to describe a small company which I think many of us has not even heard the name.

The name of the company is SIRCA PAINTS INDIA LIMITED.

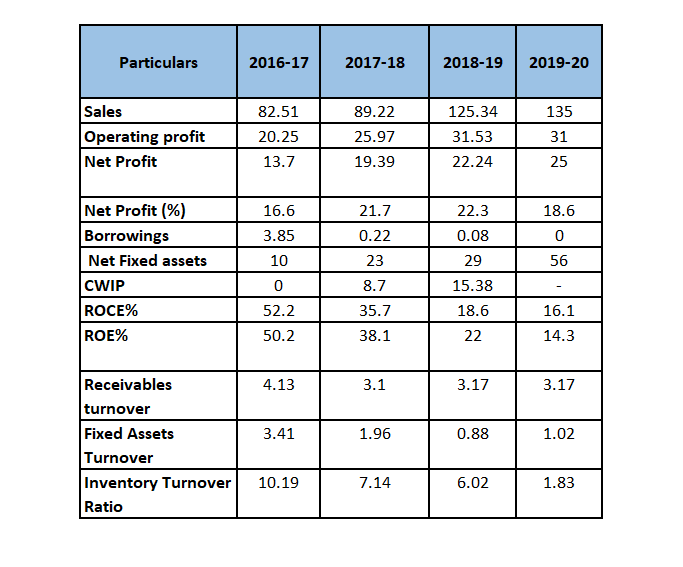

It is a very small company having a market capitalization of just 932Crs (As of 26/02/2021). Let’s take a financial snapshot.

Key Financials (Rupees in Crores)

On the financial side the company looks so strong so let’s talk about the company.

About the company:

· Sirca Paints India Limited was incorporated in 2006, It was established by Mr Sanjay Agarwal who is the present Managing Director of the Company.

· Company has its registered office in New Delhi.

· The company was engaged in the trading business of Premium wood finishing/coating, PU Products, stains, special effects, acrylic PU, Polyester, wall paints UV Products. It is a leading brand in North India but from 2019 they initiated manufacturing of paints in India.

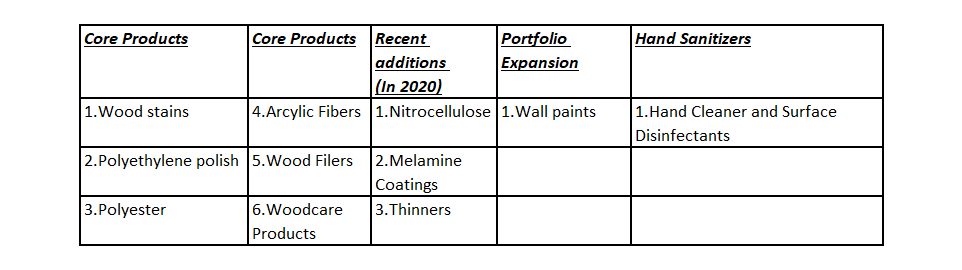

Core Products

· The company was involved in distributing and selling wood coating products. The company imports wooden coating products from Sirca SRL Italy and is the only distributor in India.

· SIRCA SRL (Italy) is also a minority shareholder of Sirca India.

· The company has a 2-decade relationship with Sirca Italy and looking for a growing market in India they entered into a manufacturing license agreement in 2018, with SIRCA SRL.

· SIRCA India also entered into Exclusive distributor rights for the country like India, Nepal, Bangladesh and Srilanka.

· Till now the story was roaming around trading and execution but they started their manufacturing in September 2019 and we can see in the snapshot that there is drastically change in the sales due to the Initiation of manufacturing and with a focus on the growth in import products as well.

· Company has established 2 manufacturing units in India during 2019 with the help of IPO proceeds (one for wall paints with 24 lakh litres Capacity) and the other for coating products and some new products (12000 tons).

· The unit for coating products is a state-of-the-art facility and whilst wall paints (7 products) unit is built on leased land and building model with minimal capital expenditure. The state-of-the-art facility for coating products has got all the necessary government approvals and started its trial production in Oct 2019.

· Having a Premium recognition, the Italy Products are saleable at a premium while capturing unorganized and increase in market share, they try to focus on reduction of the manufacturing cost and selling at a low margin and regaining margin from Trading Imported products.

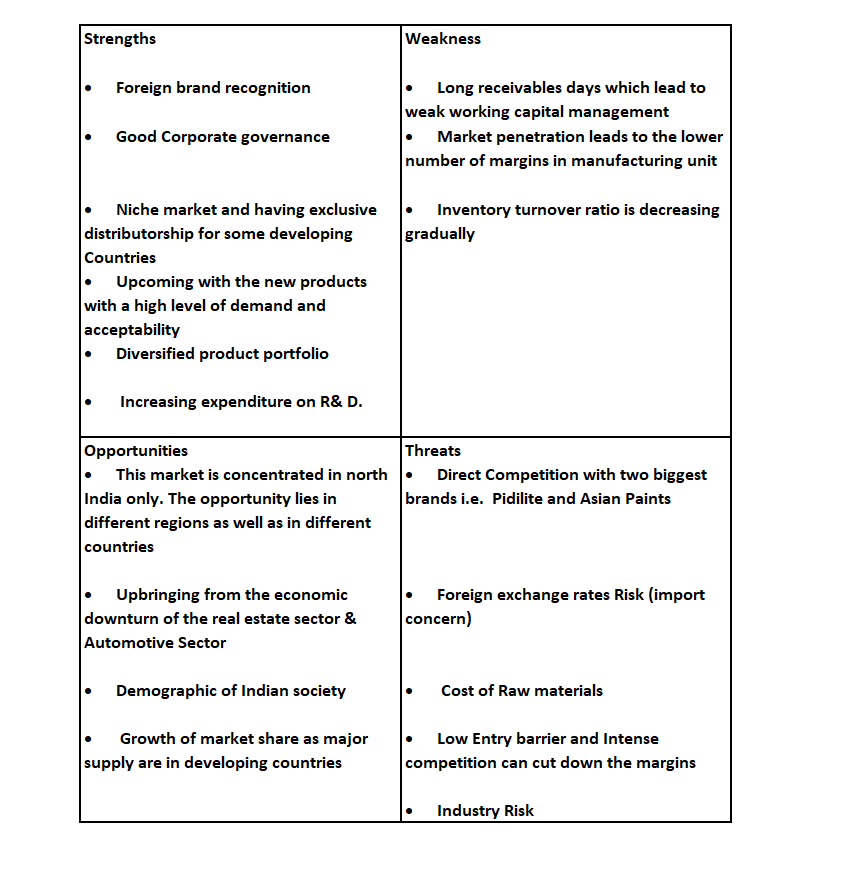

SWOT Analysis

Industry and Market Structure

· The Indian paint industry is estimated to be a 50000 crore market annually. The paint industry is mainly divided into two segments Decorative and industrial segments.

· Decorative paints constitute almost 75% of the total industry.

· Decorative wall paints consist of multiple products like exterior & interior emulsion, enamels, primer & thinner, wood coatings and other products as well.

· Industrial paints segments consist so automotive paints, marine coatings, powder coatings, Protective coatings and others. Almost 65% of the market is captured by organized players which will increase to 70-75%in the next 5 years.

· Wood coatings are used for their adhesion, anti-corrosion, durability, appearance enhancing & aesthetics features on wooden furniture.

· In the last decade, India has shaped up to be one of the largest markets for wood coatings products in the Asia-Pacific region.

· Indian furniture industry, which happens to be a key demand driver of wood coatings products, is estimated to be a USD 5 billion market in 2018-19, with nearly USD 1.5 billion in exports and USD 0.6 billion in imports.

· In the short-run paints industry will depend on monsoon which is crucial for rural demand, recovery post slowdown in the automotive sector and pickup in construction and housing demand.

· In the long run, the paint industry will grow on account of the increase in disposable income, demographics, rising urbanization, increase in nuclear families and an increase in the standard of living.

· In India, 66% of the population are under the age of 35, India is home to the largest population of young people in the world i.e., 825 Million. The median age of the country Is just 27 years, much below 37 in the U.S. and 46 in japan. India’s demographics profile is changing in a way quite favourable to the growth of the paint and coating industry.

· Indian Automotive market is the third-largest in Asia after Japan and China. The automotive paints market in India is projected to witness a growth of 10% by 2019.

· Automotive paint is highly demanded in India.

· Two-wheeler and passenger car are among the two major segments in India’s automotive paints, market roughly contributing about 75% of overall automotive paint consumption in volume.

Shareholding Pattern

Analysis

· Company has started manufacturing unit at Rai, Sonipat (NCR) having a capacity of Producing PU Thinner of 40,00,000 Lakh Liters, NC, Melamine and Economical Pu products 80,00,000 Lakh litres, Wall Paints at 24,00,000 Lakhs Liters. Which is maximizing to capture market share and formalized shifting of market share from unorganized to organized.

· Lower production costs and retail-based model helps them to gain economies of scale

for their products as well they also import their products from Italy which attract and retain the consumers which help to generate a high-profit margin and leads to the sustainability of the operating profit margin at 25%.

· Demographics, disposable income, standard of living, increase in lifestyle as well concept of the nuclear family have significantly increased the importance of interior designing and Concept of fancy walls, dining tables, wood flooring, Kitchen modules ambience increase in the consumption of the company Products.

· Company has more than 1600+ Dealers, 15 branches& depots, 11 Sirca studios and 2 manufacturing units.

· 70% of their revenue is generated from the retail segment, Other 30% of the revenue is been generated from original Equipment Manufacturers Which Represents that they don’t have a concentrated client which leads to Reduces counterparty risk and liquidity risk.

· Their marquee clients are Godrej, Jindal Stainless, Indoline, Spacewood, Pyramid, MAS furniture etc.

· They became a debt-free company in the previous year and they don’t have any financial risk of payments.

· Continuous Capital Expenditure on fixed assets and rigorous focus on R&D which leads to new product positioning and capturing the taboo and untapped market will lead to an expansion in the business operations.

· Operating profit margin is extraordinary and they are going to continue and will improve for future growth as well stated by management.

· These company had declared a dividend of 8.21% of the face value i.e., 10 Rs in the year 2018 and management promises to deliver the best performance in future as well.

· Company has a lot of potentials to grow as the industry market is booming up. They are trying to lever up with their product segment in all 4 sides of India as well as other developing countries.

· They can create a great moat of business as they have foreign brand recognition.

· They are focused on developing new products which can achieve a success ratio which can lead to a better story in the next few years.

· Inventory and trade receivables are high due to economic condition. Management stated they have made their credit cycle period low and trying to increase a new credit cycle system which helps to reduce inventory and trade receivables days soon.

· Management is hands of young blood and lots of entrepreneurship spirit of Mr Approov Agarwal with in-depth experience and knowledge of this industry of Saurabh Agarwal helps in massive growth for the business.

· SIRCA industry has shown a revenue growth Significantly from FY 16-Fy 20 At 17.7% CAGR i.e., 70Crs to 140Crs, While the Profit margin also grew significantly at 36.68% CAGR from FY 16- FY20 I.e., 7.27 to 25.15 crores.

· They became a debt-free company in 2019 and management is going to be debt-free for years from now.

· Average 3-year Return on Equity is 28.5% CAGR and the Average 3-year Return on capital employed is 20.3% CAGR.

· The business has a good moat, niche market and especially a recognizable brand which can lead to boost the revenue for next few years and have good profit margins can show up good growth in the company.

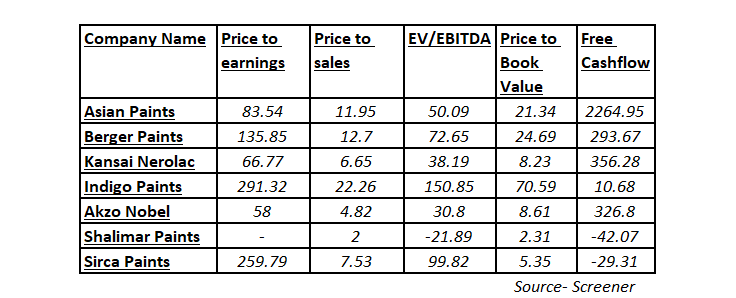

Relative Valuations

· In relative value comparison, we can see that circa paint is trading at a PE of 259.79 which we could say the earnings has decreased on a large scale as a major portion has the income is spent on marketing and increased in the dealership and Covid 19 effect has tightened up the margins and squeezed the profit part but on an overall part, you can see that price/sales and price/book value is comparative good, comparing with indigo paints and Berger paints.

· Valuation seems decent in relative terms while Shortly the company will deliver a good profit which will lead to a decrease in Price to Earnings.

· Free cash flow is negative because a major part of the cash flow is been spent on expansion and advertising to increase the recognition of the brand.

Comments

· SIRCA looks truly a growth stock, the only risk concern with it is competitiveness and fear of industry, for the next few years’ industries will go on a good state as proactive decisions taken by and bold moves been taken by our government to regain that GDP growth, while only risk and concern are industry rivals.

· SIRCA has a good command in north India for its brand which ultimately can be a good moat for the business and presence in a niche market can have a low downside risk for revenue degrowth and being leaders in wood paints and PU which also helps the company to achieve economies of scale and can maintain with low cost and delivering good quality of the product in long-term prospects.

· In my point of view, we should wait for the next one or two quarters for the performance report before we move to buy indication, as there is an uptick in demand in the real estate sector on which help in a boost in the revenue.

· The only major concern is PE and providing such a high valuation for such a company can be a disaster in long term. Earnings based adjustment in PE can construct a good value buy for the long term as we can get a cushion for the margin of safety.

Thanks For Reading,

EquityManiac.

If you like our analysis please follow for such analysis. Please share with your friends and discuss is this company is worth to invest or not. We will be back with such a short analysis until then...

just wanted to know that these wood coatings are not for giving colour to wood i guess. It is applied on the wood to make it more protective and add more shine too the existing colour